"About 80% of what those R&D people do have nothing to do with writing code [in software companies]." says Orlando Bravo, co-founder of Thoma Bravo, the firm that has bought and sold more software companies than anyone in history.

What is that 80% then? It is the decades of industry knowledge, accumulated record of business decisions and underlying reasoning, thousands of existing connections to other software, industry-specific regulatory expertise, and the built-up trust of large enterprises. Not a static pile, but a live knowledge base that continues to evolve with ongoing customer and industry engagements.

So where does this accumulated knowledge actually live?

Matt Brown at Matrix Partners calls it the context graph — the queryable record of business logic, decision traces, and reasoning that explains why things happened, not just what happened.

Matt provides an example from Toast, a restaurant management software platform. Toast's data model has objects like Order, MenuItem, Customer, PrepStation with built-in relationships. Connect inventory to orders and you see demand patterns. Connect customers to inventory and you see which stockouts hurt your best buyers. Connect payments to all of it and the full economic picture comes into focus. Each layer of context makes the previous layers more valuable. When the data model is opinionated enough, you get inferential density. Each new function added to the graph makes everything already in the graph more meaningful. The graph doesn't just get wider. It gets denser. And when it's dense enough, the "why" becomes reconstructible from the relationships between nodes — without anyone having to explicitly log the reasoning.

The same principle applies at massive scale. Facebook and Google have full visibility of the advertising value chain — ad targets, ad buyers, publishers — each layer making the others more predictable. Extreme inferential density.

That density is the moat. Not the code. Not the interface. Not the raw data. The accumulated recipe of how the customer businesses actually work.

Epic doesn't sell patient records — it sells the recipe for billing across 47 payer edge cases in 12 states while maintaining HIPAA audit trails. Procore doesn't sell project files — it sells the recipe for how a change order flows from field to office to invoice to lien waiver. Veeva doesn't sell a document repository — it sells the recipe for how a drug navigates from clinical trial to regulatory approval across three countries with three different submission frameworks. Each recipe took years of domain expertise to encode. It consists of thousands of edge cases, accumulated and structured, after decades of observing, listening, and learning.

Code is the delivery mechanism. The codified industry knowledge is the actual software.

The last mile isn't the final brief stretch at the end of a long road. It is the road.

Software businesses' extensibility challenge

The diversity of the real world — industries, geographies, regulations, organizational cultures, the seventeen ways a hospital in the Netherlands differs from a hospital in Texas, makes it impossible for any single software to serve all customers out of the box. There's always a gap between what the software contains and what the business needs. This gap, i.e. "the last mile", can be:

- Configuration: the settings, parameters, and rules that tell software how a specific business works. Chart of accounts, approval hierarchies, pricing rules.

- Integration: wiring the software to APIs, middleware, data pipelines, the other systems it needs to talk to. Often the largest cost center and the least visible.

- Customization: adapting workflows, interfaces, and logic for distinct industries, geographies, and regulatory environments.

- Infrastructure: hardware, security, performance, disaster recovery.

- Operationalization: training, change management, the human processes that wrap around the software to make it actually function in an organization.

Vercel is a simple illustration of how business moat is built on the removal of these "last mile" burdens. Every step in a developer's front-end deployment chain — CI/CD pipelines, preview environments, edge functions, SSL certificates, CDN configuration, domain management — is individually straightforward. Any competent engineer can set each one up. But the totality of doing all of them, maintaining all of them, keeping all of them coherent creates a cognitive fog that bleeds into the actual product work. Vercel didn't invent every capability in that chain. It made the cognitive load of the entirety disappear. Simple action and your web is live. The value isn't in any one thing Vercel does. It's in the mental space reclaimed when you no longer have to hold the whole chain in your head.

This is why every software company must choose an extensibility strategy: a deliberate approach to bridge the gap between their system and reality. Their extensibility bridge determines their economics, competitive position, and resilience against technological and/or commercial disruption.

Here is how I see these strategies in four categories:

1. Dev ecosystem: provide infrastructure for external builders to create new value on top

For every $1 Microsoft earns, the ecosystem generates $7.5 (service-led) to $10 (software-led). Therefore, Microsoft doesn't ship finished enterprise products. It ships a developer ecosystem. Windows, Azure, Office 365, Dynamics — these are platforms that provide perhaps 70% of the solution. The remaining 30% gets built by a vast community of 400,000 partners, and internal IT teams working across the .NET ecosystem.

This is a deliberate design choice. The product is designed to be completed by someone else, like a franchise chain where the central kitchen develops the menu, the recipes, and the supply chain, but each location does the final preparation for local taste and local regulation. Not because headquarters can't cook, but because the finishing is where local context matters.

Google and AWS ecosystems also generate $7 and $7.13 per $1 of Google and AWS sales.

At the application layer, Salesforce's ecosystem is the largest with 3,400 consulting firms, 170,000 certified experts, making $6.19 for every $1 Salesforce earns. 9 out of 10 Salesforce customers rely on partner apps or external experts. The company is perceived as having the lowest entry barrier, but it still has 78% gross margin and 8% gross churn. Anthropic, OpenAI, Google and Amazon use Salesforce, and even Anthropic was looking for Salesforce Administrators as recently as last week.

ServiceNow has been a modular, cross-system layer within the enterprise software stack. Partners can build workflows on top of the routing and governance that ServiceNow already provides. Attractive infrastructure for dev ecosystem. The company has 2% gross churn rate, one of the best at scale, despite not being a system of record.

Overall the economics are critical: the partner builds something, sells it to many customers, and the underlying platform gets utilized with every extension. Each addition makes the ecosystem more valuable for everyone else. The platform's value grows exponentially with ecosystem size.

This developer ecosystem strategy is a structural requirement at large scale. OpenAI's Frontier Alliances demonstrates exactly the same pattern for AI-native companies: multiyear deals with McKinsey, BCG, Accenture, and Capgemini, each building certified practice groups and dedicated teams around OpenAI's Frontier platform. Strategy partners (McKinsey, BCG) help leadership rewire operating models; implementation partners (Accenture, Capgemini) handle data architecture, cloud infrastructure, and legacy system integration. OpenAI's own forward-deployed engineers work alongside them. Early enterprise customers include Intuit, State Farm, Thermo Fisher, and Uber. The consulting firms are the capillaries; the platform is the artery. No trillion-dollar-plus software company has reached that scale without this circulatory system.

2. SI ecosystem: external navigators fit an over-engineered system to the customer

SAP's approach, and Oracle's and Workday's, is structurally different. Build a system so comprehensive that every conceivable business process is somewhere inside it. The customer's job is to figure out which 20% they need and configure that subset to match their operations.

This figuring-out process is itself a multi-year, multi-million-dollar undertaking. Whether it is success or failure, making the system work takes years, tens of millions of dollars (Lidl: €500 million over 7 years on a failed SAP implementation), hundreds of dedicated employees (Mettler-Toledo: 18 years. $661 million in capitalized software costs. A 585-person Shared Business Center in Warsaw.). This is where the systems integrators come in — Accenture, Deloitte, TCS, Wipro, the entire IT services pyramid. Their job is navigation: guiding customers through a comprehensive system to find and activate the right capabilities.

These are not byproducts but a deliberate extensibility strategy. SAP designed for this deliberately with certification programs, partner tiers, implementation methodologies (ASAP, Activate), reference architectures.

The SI configures the same system from scratch for each customer. Revenue scales with headcount. No compounding. No leverage. There's a structural incentive to maintain complexity: the SI doesn't want SAP to become easier to configure. That's their revenue.

Directionally, SI work and the revenue pool are crumbling. Workday GO deploys in 30-60 days versus traditional 8-14 month implementations. Master Builders Solutions went from kickoff to go-live in 42 working days. Navigation work — finding the right 20% in a comprehensive system — is compressing from years to months to weeks.

While this should be beneficial to the incumbents, when a product has been built for decades around the assumption that external navigators will spend months configuring it, that assumption doesn't just live in the ecosystem — it flows into the core product architecture. Data models, integration patterns, permission frameworks, deployment pipelines — all designed for a world where complexity was someone else's revenue. To a great extent for SAP and to a lesser extent for Oracle, the underlying architecture still assumes the SI. Decoupling from that assumption means re-architecting the product, not just adding a copilot.

On the other hand, Workday having cleaner foundations can move faster. Workday's CTO Peter Bailis — who left Google Cloud for Workday specifically because of its unified data model across 11,000 customers — is building exactly this: an extremely granular framework that extends the org chart's permission model to AI agents, an Agent System of Record, and open agent-to-agent protocols included in the base SKU at pay-as-you-go pricing. The architecture was built for a single data model. Agents slot in.

Notably, Palantir is the exception to the staleness of the industry. By owning the SI layer, the incentive flips: compress implementation, grow faster. When the vendor outsources the SI layer, the incentive is perverse: maintain complexity, protect ecosystem revenue. Palantir's AI FDE (Forward Deployed Engineer), launched November 2025, replicates much of what human forward-deployed engineers do. The AIP Bootcamp compresses the 3-12 month enterprise sales cycle into 5 days. 70% revenue growth. FY2026 guidance of 61%, nearly $1 billion above consensus.

3. Focused vertical product: product accounts for the last mile

By focusing on domain, some vendors pre-solve the last mile extensibility problem.

Toast provides a working restaurant management system on day one. Different feature sets for a food truck versus fine dining. Different POS hardware integrations. Different state compliance modules. The "config" was handled by product design: the company anticipated the variations and built them in.

The pattern repeats across verticals. Veeva pre-solves pharma industry workflows across therapeutic areas and countries. Guidewire pre-solves insurance administration. Procore pre-solves construction workflow from field to office to invoice to lien waiver. AppFolio pre-solves property management from leasing to maintenance to owner reporting. Samsara pre-solves fleet and facility operations with sensor-to-software integration across 95%+ of $100K+ customers on two or more products. Intuit pre-solves tax and accounting logic for 100 million consumers and small businesses. Add Synopsys and Cadence (semiconductor design), Autodesk (architectural and engineering workflows), Dassault/PTC (engineering and manufacturing), and Amadeus/Sabre (airline, airport and hotels).

The composable vertical product isn't just narrower, it's opinionated. It ships with the institutional knowledge baked in. Pre-built industry workflows, curated data, best-practice templates, expert decision logic, compliance rules. Content-rich software where the meaning is already there, not bare-bones software that the customer must fill.

This works because the commercial-product development loop is tight. Customer success teams learn what breaks in the field, feed it directly to product, and because the domain is narrow, releases land. But CS teams also decipher customer frustrations and identify adjacent fields to expand into.

4. Internal company layer: the customer absorbs the gap

The fourth model is where the customer bridges the gap with their own people.

MS Excel, Monday, Asana, Airtable, Notion, Smartsheet, Coda. These products sell the gap as a feature. Here's a flexible canvas, structured enough to be useful, open enough that you configure it into whatever your team actually needs. The tradeoff is deliberate: maximum flexibility, minimum opinion. The customer brings the domain knowledge.

The spreadsheet is the purest such product ever built. Zero opinion. Infinite flexibility. The user supplies all the meaning. It is no coincidence that "Stop running your business on spreadsheets" was the enterprise software pitch of the 2010s (now ironically it is "Let me help you use spreadsheets more easily.").

This is the category with the harshest churn, lowest switching costs, most competition, severe lack of differentiation, and lowest entry barriers. Some of these products may have somewhat replaced the spreadsheet's interface but not its structural problem: the customer still supplies all the domain knowledge. Still configures every workflow. Still maintains the logic. A prettier empty canvas is still an empty canvas. The canvas was the config. Remove the config, and the canvas has no reason to exist. An agent that can manage your project doesn't need a project management tool to manage it in.

They have the tightest survival path: stop selling flexibility, start shipping business logic. Monday.com's fastest-growing products aren't the flexible board — they're Monday CRM, Monday Service, Monday Dev, vertical modules with pre-built logic for specific functions. Monday Vibe, a custom app builder on Monday data, hit $1M ARR in 2.5 months. But the pivot is from a position of weakness: growth decelerated to 25%, 2026 guidance cut to 18-19%, 2027 target dropped entirely. Airtable's CEO went further — launched Superagent, the company's first standalone product in 13 years, a dedicated AI agent platform. After a decade building the most flexible canvas on the market, the founder's next bet is a product that makes canvases unnecessary.

Agent runtime: collapsing the last mile

Too much focus goes to software creation getting faster and cheaper.

The real shift is: malleability.

Traditional software, compute runtime, is deterministic. It has rigid instructions, edge cases it can't handle, integrations it can't make without months of middleware, data it can't accept unless you decompose it into the right fields. The software is a fixed shape. The business has to contort itself to fit. It requires a lot of engineer hours, back and forth communication with end users, and change requests and re-engineering cycles before it becomes truly useful in the real world.

Agentic runtime adapts. It takes voice, text, video, a screenshot of a whiteboard, and figures out the structure itself. It resolves edge cases that were never explicitly programmed. It reasons across systems without custom integrations. It conforms to the business instead of requiring the business to conform to it. Years of engineering versus one week of writing a procedure in English.

For instance, Procore's superintendent walkthrough can capture the full story of a construction site. An agent analyzed job-site video, identified an incorrectly coded column, pulled the relevant drawings and specifications, created a rework order, and halted downstream work — hours of manual expert navigation reduced to one prompt.

Building a dense context graph — the kind Toast, Epic, or Procore accumulated over years — traditionally required mega-systems: massive data collection, years of integration work, thousands of encoded edge cases layered until the graph became rich enough to reconstruct the reasoning behind business decisions. Atomic agentic runtimes offer a different path to density. Not through accumulation, but through connection. A well-resourced agent runtime, wired into the right APIs, databases, documents, and live context, synthesizes inferential density just in time and with small data. No massive data pipeline behind it. No years of painstaking integration. The agent constructs the inference at the moment of need, within the scaffold of its own runtime, by reasoning across whatever is available. But the quality of that synthesis depends entirely on what's behind the connection. An agent wired into Veeva's drug safety system reasons with eight years of regulatory knowledge across every therapeutic area and country. The same agent wired into a generic database reasons with nothing. Just-in-time density is a capability of the runtime. Accumulated density is the asset that makes it valuable.

Agentic runtimes collapse the software's "last mile" gap, and that gap is where the most value has been trapped.

Terrain

Enterprise AI has surged from $1.7 billion to $37 billion since 2023, capturing 6% of the global SaaS market and growing faster than any software category in history (Menlo Ventures). 76% of AI use cases are now purchased rather than built internally. 70% of AI builders are focused on vertical applications (ICONIQ).

The past six months provided a natural experiment. Despite a broad software selloff, the companies continued to perform well (see Appendix for the latest earnings).

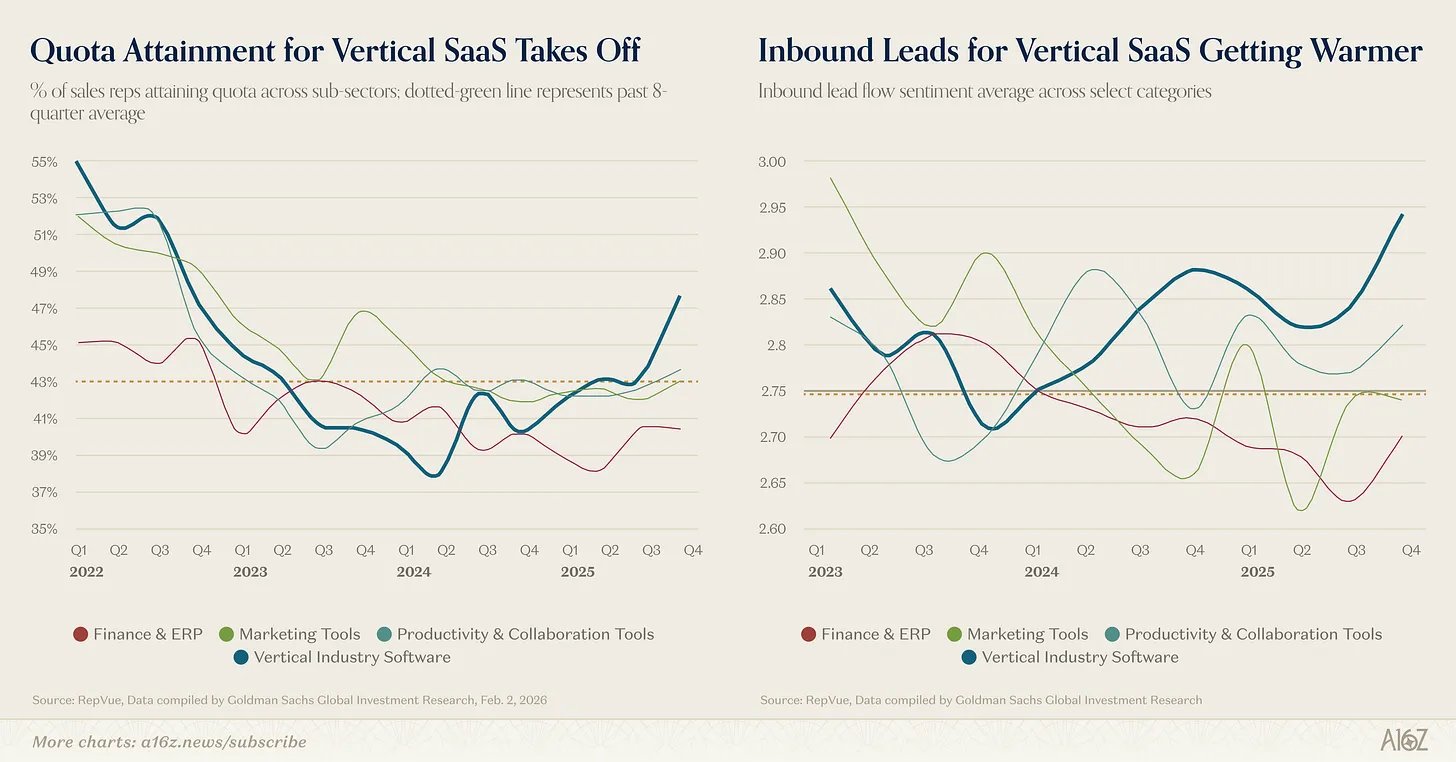

Goldman Sachs data (compiled from RepVue, Feb 2026) confirms it from the sales floor: vertical industry software quota attainment surged in Q4 2025 — above productivity tools, marketing tools, and finance & ERP, all of which stayed flat or declined. Inbound lead sentiment for vertical SaaS spiked to its highest level in three years while every other category flatlined.

The financials tell the story of the past. What matters is how each extensibility model might change when AI compresses the last mile. The same force hits each model at a different angle.

Future

1. Incumbent Vertical SaaS has asymmetric positioning advantage. These companies were already winning the last mile with the highest inferential density and the deepest domain knowledge. AI widens the gap.

Menlo Ventures data shows product-led growth (PLG) drives 27% of AI app spend — 4x the rate of traditional SaaS at 7%. PLG works when the product solves the problem without requiring a sales process, an implementation team, or months of configuration. When the software already knows how the domain works, there's no abstraction layer between user and outcome.

Capacity to build software has massively expanded. Capacity to learn an industry is still an extremely scarce resource, especially at scale. Domain expertise is not a static asset. It is the organizational muscle to learn from an industry continuously — to absorb what customers struggle with, feed it back into the product, and reshape how the industry operates. When that muscle atrophies — when the people leave, the relationships go transactional, the product stops evolving — the knowledge dies even if the code still runs. The distinction is not between companies that have domain knowledge and companies that don't. It is between companies where the knowledge is alive and compounding, and companies where it once existed but nobody maintained it.

For instance, Oracle acquired Cerner for $28.3 billion in 2022 — the second-largest healthcare IT company in the world. In 2024 alone, Oracle lost 74 hospitals and 17,232 beds; Epic added 176 hospitals and 29,399 beds. Half of customers said they would not purchase the EHR again. Before acquisition, Cerner had 12,778 employees in Kansas City. Oracle cut this to 6,400. The domain expertise that made Cerner valuable was not in the code or the data model. It was in the people, their relationships with clinicians, their understanding of clinical workflows. Remove the people and the knowledge dies, even if the product still runs.

On the other hand, enterprise adoption has a structural gate that compounds the incumbent advantage. Authentication, authorization, and procurement checklists aren't formalities. They're months of security reviews, vendor approvals, SOC 2 audits, SSO integration, and legal sign-off. Every new vendor goes through this. The incumbent doesn't. The gate isn't unbreakable, but it gives incumbents a head start on capturing the volume as enterprises warm up to agentic workflows. The path of least resistance is the system that's already passed procurement.

Vertical SaaS vendors are in the sweet spot of these two forces. The former fends off horizontal players; the latter, the emerging vendors.

The result?

- Valuable time to create agentic products without extreme urgency. 2% annual gross churn approximately means 50 years of customers (ServiceNow, Tyler, Workday, Datadog); 5% means 20 years (Veeva, Procore, Cadence, Synopsys, Amadeus — some are estimated); but 8% (Salesforce, Monday.com) means 12.5 years. Anything above 5% opens doors to emerging players. Combined with low NPS (35 for Salesforce), it becomes a growing statistical force for market share compression. Customer acquisition can compensate, but that gets harder against agentic products that demonstrate value in days, not months. Unless the incumbent has unique data leverage or genuine insight into how the customer operates (e.g. public markets data, legal data, domains where the underlying information is accessible to anyone), higher churn and lower differentiation will lead to margin squeeze.

- Visibility advantage. Customers feel close enough to vertical SaaS vendors, to share what actually breaks in their operations, and product development stops being speculative. You don't survey the market — you hear it directly, continuously, from the same customers year after year. That is why vertical SaaS companies expand into adjacent products with high hit rates. The vertical players already know what the customer struggles with next. Horizontal players and new entrants guess.

- Operationalization flywheel. The installed base is a substrate for product experimentation, faster and interconnected deployments, a growing context graph, and even more product ideas. AppFolio's 98% AI feature adoption — while 78% of the broader industry says they cannot rely on AI in their legacy software — is the flywheel in motion. AppFolio reasons over 9.4 million rental units of operational data that AppFolio already has, filling rental units 5.2 days faster, increasing renewal rates 20%, saving 12.5 hours per week. A new entrant ships the same capability into a vacuum.

Caveats?

The first is data architecture. The architecture determines whether a company can learn across its customer base. Single-instance platforms or well-designed multi-instance ones (ServiceNow, Guidewire) will enable pattern recognition across all customers. Siloed or on-prem customer data without a well-abstracted data layer offers no differentiation. The context graph requires not just data generation but also accessibility. Some vertical SaaS companies sit on years of customer data they structurally cannot use.

The second is organizational nerve. Having the static advantages means nothing if the organization cannot take risks. Leadership willing to cannibalize current revenue (including per-seat pricing) for future positioning can unlock more rewarding business models. Companies paralyzed by quarterly earnings pressure or cultural inertia won't. A software company that has not yet instituted agentic product development standards is already significantly disadvantaged.

The third is technical debt. Agentic coding compresses the product cycles, but that only works if the codebase can absorb it. Legacy architectures with decades of accumulated tech debt cannot move at that speed regardless of how good the insight is. The company may know exactly what the customer needs and still take two years to ship it. Alive knowledge without a modern codebase is a car with a great engine and no transmission.

The agentic transition is not like the cloud transition. When computing was moving from on-prem to cloud, the on-prem vendors had no customer data, no usage visibility, no relationship beyond the initial license sale. The infrastructure-to-application capital flow will repeat (it always does), but today's application software incumbents will start with proximity to customers and data already flowing through their systems, available for further product development.

2. New customers: Agents. Pricing will follow. Usage will explode. Over the past two decades, the best software companies built shared infrastructure for their industries. When these companies expose their context or data as transaction layers — APIs, MCP endpoints, agent-accessible protocols — they detach from the human interface entirely. The infrastructure persists. The screen becomes optional. And when agents start transacting, they will exceed human transaction volumes.

Every market that removed the human from the transaction loop saw the same result. When the CME launched Globex, futures volume went from 1 million contracts per day to 28 million — a 28x expansion over two decades. US equity markets went from 12 million shares daily in 1970 to 12.2 billion today. Electronification doesn't transfer volume from human to machine; it creates an order of magnitude more volume, because machines transact at speeds and frequencies humans never could. When frictions fade, actions become more frequent. That is why merchants pay 2% on every credit card swipe as users spend 83% more per transaction than cash users. The fee is the price of access to a higher-velocity transaction layer.

Humans pick from the few vendors they know under time pressure. Agents can discover hundreds, from anywhere, evaluate all of them, and make them compete — turning every business decision into a broader, faster, higher-volume transaction surface than human-scale commerce ever allowed. Aaron Levie, the CEO of Box, believes agents could increase US enterprise software spending from $100 billion to $250-400 billion — based on agents capturing 5% of $5-8 trillion in knowledge worker salaries. There are ~100 million knowledge workers in the US, and 1.25 billion knowledge workers globally, implying a $1 trillion plus market. This still does not account for the transaction volume uplift in B2B business processes. The enterprise software companies building for agents will capture the lion's share of that incremental spending.

One implication of such terrain is that the competition becomes merit-based. Amadeus, Travelport, and Sabre all competed for the same complex flight bookings flow on Expedia. Amadeus has steadily gained share not through branding or interface design, but through response time, inventory breadth, and connection reliability. Pure infrastructure merit. The traveler does not even know. The agent doesn't care who you are. It routes to whichever system returns the best result fastest.

That is likely the future of software distribution: targeting agents as the main users. The companies have already started to build for agents:

- Shopify's Universal Commerce Protocol ensures any AI agent can transact through Shopify infrastructure without ever seeing a storefront — orders from AI search increased 15x since January 2025.

- Datadog's MCP server got 11x more usage in its first week than Terraform (popular developer tool) accumulated in its entire first year. Agent-driven adoption velocity dwarfs even developer tool adoption.

- Atlassian's MCP server is already how Anthropic's CoWork accesses Jira and Confluence — millions of agentic workflows run monthly.

- Palantir serves over 1 billion API gateway requests per week from agent-built applications.

- Stripe launched a protocol for machine-to-machine payments, without a checkout page or human involvement. Stripe and Paradigm also incubated Tempo ($500M raised, $5B valuation), a payments-first blockchain designed as the credit card network for agents.

These companies are not building for screens. They are building for agents. If agents are the users, API access is the distribution channel. Yet the large data aggregators, from Nasdaq and Factset to Booking.com, still gate their APIs with approval processes, charge thousands for integration setup, or over-engineer endpoints to the point of friction. When enterprise agents orchestrate processes across ten systems, the system that blocks API access or silos its data doesn't get worked around — it gets replaced. Open, fast, and high-quality API endpoints are no longer a nice-to-have. API access is the growth channel, or the churn trigger. Lose API, lose usage, lose subscribers.

Pricing follows the same logic. When the customer is an agent completing work, per-seat licensing loses meaning. Already 37% of companies plan pricing changes within 12 months (ICONIQ). Even notoriously outcome-detached services are transitioning. McKinsey now generates a quarter of its global fees from outcomes-based pricing. Workday now prices agent API calls at a premium, because each one completes work that used to require a human. The pricing follows: a call that resolves an HR case or closes a ledger gets priced like the work it replaces, not like a database query.

For that reason, companies like Salesforce might have a rough patch in the inevitable transition away from per-seat licensing. The transition will certainly create a revenue gap and margin dip. In the worst case, Salesforce becomes a headless CRM as a system of record, with agents rewiring workflows instead of configuring screens, reducing the company to platform-as-a-service with significantly lower margins. It is not only a Salesforce problem, per-seat to outcome/value based pricing shift is also discussed in Dassault, Asana, ServiceNow, Cadence, and Workday earnings. Transition away from per-seat pricing will make these companies very execution-dependent with a wide variety of outcomes, since it is essentially a change in the business model and income statement, and requires sustained execution to navigate.

3. The dashboard is not dead. Moving up from the audit and configuration layer to the orchestration and communication layer. Exposing the infrastructure as a protocol doesn't collapse the software to a dumb endpoint. New layers emerge on top, layers that didn't exist when humans were the bottleneck.

The agentic system is best utilized as an autonomous system working asynchronously. When a human recruiter screens candidates, they process perhaps 50 CVs per week. An agentic recruiter processes 5,000 per day — sourcing, matching, ranking, scheduling, without a single screen being opened. It's a categorically different volume of work that was never economically viable before. Set once, it runs thousands of times — carrying the embedded memory and preferences of the business it serves. For that reason, there need to be at least three new software layers to accommodate the human-agent composite workflows:

1. Agentic work review. Autonomy doesn't mean zero human involvement. It means humans shift from doing the work to reviewing the final bit. An external agentic recruiter sends 200 candidate packages, internal agentic recruiter reviews and accepts 50 candidates, the system pays for the work, the hiring manager reviews, accepts three, the system pays for the placement. Similar pattern with agentic customer service or ad buyer layers. This review-and-pay loop is itself a new product layer. Especially the vertical SaaS companies owning the domain context are best positioned to build a trustworthy review surface, because they know what "good" looks like in that industry. At scale, this review layer becomes governance, ensuring that the decisions are compliant, coordinated, traceable, and reversible.

2. Recipe generation interface. Autonomous work runs asynchronously, without a human operator. The software executes recipes thousands of times, unburdened by human throttle. At an architectural level, business goals, directions, and limits get encoded as flows — a connected set of actions, conditions, and rules that is wired together as the complete business system design that can be drilled into for task-level audit when required. The vertical SaaS companies with the highest inferential data density own the best means to create such recipes.

3. Control plane. Today, agents work in series — one task, one prompt, one human in the loop. The near-term shift is synchronized parallel work: a developer directing five agents simultaneously (Cursor's cloud agents already produce 35% of merged PRs this way), a procurement manager overseeing ten supplier negotiations at once, a compliance officer reviewing outputs from fifty concurrent audits. Humans still orchestrate. But that is a transitional state. The end state is legions — thousands of agents spawned in parallel, each executing a fragment of a larger objective, communicating with each other, resolving conflicts, and converging on outcomes without a human relaying messages between them. A construction firm running 10,000 daily compliance checks across every active job site. An insurance carrier reprocessing 50,000 claims overnight when a regulation changes. At that scale, human orchestration is not just impractical — it is impossible. That requires a control plane: the infrastructure layer that provisions agent fleets, routes them to the right context, manages their communication channels (eg. Agent Relay), and governs their collective output. When the unit of work shifts from "one agent, one task" to thousands of always-on, communicating agents with ongoing objectives — the software that orchestrates those fleets becomes a platform layer in its own right.

These layers (and maybe more) are where the next generation of added-value lives in software.

Agentic runtime is a new type of compute — human-equivalent work delivered programmatically. We cannot staff thousands of people overnight, but we can provision millions of agents instantly. This will change what enterprise software is, at a faster pace than the on-prem to cloud transition. Incumbents can benefit as much as emerging players, so long as they have accessible data with high inferential density and strong customer relationships. But it is not a given — organizational inertia or ecosystem dependencies that profit from complexity can inhibit the transition. Per-seat pricing will become defunct, creating revenue gaps and margin compression — transitory pain for some, permanent for others.

Vertical SaaS companies are particularly well positioned: their data density means agents run with domain knowledge that horizontal systems cannot replicate. As each unit of human-equivalent work gets cheaper and frictionless, usage volumes will explode. And as agentic operations become the norm, software will need layers that don't exist yet — orchestration, review, recipe generation, control planes, built by the companies that already know what "good" looks like in their industry. The last mile collapses for those who know exactly how to build it and are nimble enough to move fast.

Appendix

Latest reported earnings (as of Feb 2026):

| Company | Period | Rev Growth | Comment |

|---|---|---|---|

| Dev Ecosystem | |||

| Microsoft | FY26 Q2 | 17% (15% cc) | Azure +38% cc; Cloud +24% cc |

| Alphabet | FY25 Q4 | 18%; Cloud +48% | Cloud backlog $240B (2x+ YoY); AI model rev ~400% YoY |

| Amazon | FY25 Q4 | AWS +24% | AWS $142B ARR; Bedrock ARR (+60% QoQ) |

| Shopify | FY25 Q4 | 31% (29% cc) | Merchant Solutions +35%; MRR +15% |

| Atlassian | FY26 Q2 | Cloud +26% | RPO +44%; NRR 120%+ |

| Cloudflare | FY25 Q4 | 34% | RPO +48%; CRPO +34%; NRR 120% |

| Composable Vertical | |||

| Guidewire | FY26 Q1 | 27%; Sub & support +31% | ARR +22% |

| Toast | FY25 Q4 | ARR +26% (FY); SaaS ARR +28% (Q4) | NRR 109% (SaaS) |

| AppFolio | FY25 Q4 | 22% (Q4); 20% (FY) | |

| Veeva | FY26 Q3 | Q3 revenue $811M | |

| Procore | FY25 Q4 | 15.6% (Q4); 15% (FY) | CRPO +22%; $1M+ ARR customers 115 (+34%) |

| Intuit | FY26 Q2 | 17% | 3M+ customers using AI agents; 237M transactions auto-categorized in Jan |

| Samsara | FY26 Q3 | 29%; net new ARR +23% cc | NRR 115% |

| Synopsys | FY25 Q4 | Record $7.05B (FY) | |

| Cadence | FY25 Q4 | 14% (FY) | Backlog $7.8B (record) |

| Autodesk | FY26 Q4 | 14% cc (ex NTM) | Billings +30% cc |

| PTC | FY25 Q4 | ARR +8.5% cc | |

| Amadeus | FY25 Q4 | 9% cc (FY); Q4 +10% | Lufthansa/AF-KLM/BA adopting Nevio, AI-native personalized offer software |

| Sabre | FY25 Q4 | Air bookings +4% (Q4) | agentic APIs + MCP server for travel |

| Dassault | FY25 Q4 | 4% cc (FY); Q4 +1% | moving to value-based AI pricing |

| Horizontal SaaS | |||

| Salesforce | FY26 Q3 | 9% (8% cc) | CRPO +11%; revenue attrition ~8% |

| ServiceNow | FY25 Q4 | Sub +21% (19.5% cc) | RPO +22.5% cc; CRPO +21% cc; renewal rate 98% |

| Datadog | FY25 Q4 | 29% | RPO +52%; CRPO +40%; GRR mid-to-high 90s |

| Snowflake | FY26 Q3 | 29% (product) | RPO +37%; NRR 125% |

| SI Ecosystem | |||

| SAP | FY25 Q4 | 11% cc (FY); €36.8B total | Cloud backlog €77B (+30%); Cloud ERP +32% |

| Oracle | FY26 Q2 | 13% cc | 12-mo RPO +40%; Cloud +33% cc; Cloud infra +66% cc |

| Workday | FY26 Q4 | Sub +16% (Q4); +14% (FY) | CRPO +15.8%; GRR 97% |

| Palantir | FY25 Q4 | 70% (Q4); 56% (FY) | RPO +144%; NDR 139% |

| Internal Company Layer | |||

| Monday.com | FY25 Q4 | 27% (FY; $1.232B) | NDR 110%; GRR 91% ($50K+ cohort) |

| Asana | FY26 Q3 | 9%; $100K+ customers +15% | RPO +23%; NRR 96% overall, 97% core |

- CC: constant-currency.

- RPO: remaining performance obligations — contracted future revenue not yet recognized; a forward demand signal.

- CRPO: current RPO — the portion of RPO expected to be recognized as revenue within 12 months.

- NRR / NDR: net revenue retention / net dollar retention — revenue from existing customers this year vs. last year, including expansion and churn; >100% means the installed base is growing, <100% means it is shrinking.

- GRR: gross revenue retention — revenue retained from existing customers before any expansion; pure measure of churn.

- ARR: annualized recurring revenue.